Standing waters — the crisis of congested entropy in our global economy

Part 1 of 3: How the IT-revolution expanded informational liquidity, and drowned it as well.

This article is just an attempt to make sense of our current global crises by looking at them from very high abstraction levels, to explain how we got here.

Let me begin with a few lists concerning our global economy:

- Unprecedented financial policies in place for almost a decade now:

- quantitative easing (Fed, ECB, Bank of Japan, Bank of England)

- zero/negative interest rates (ZNIRP)

2. Unprecedented trends and creativity because of the global yield crisis:

- passively managed assets overtake actively managed assets in value (US)

- high-frequency-trading is entering new markets, like commodities

- all kinds of new peripheral bubbles (local housing bubbles (UK, AUS, CAN, ..), student-loans, car-loans, etc.)

3. Other worrying aspects:

- crypto-goldrush (bizarre ICO’s, speculating with cryptocurrency lending, blockchain-hype, etc), with the same wild-west profile as dotcom-bubble

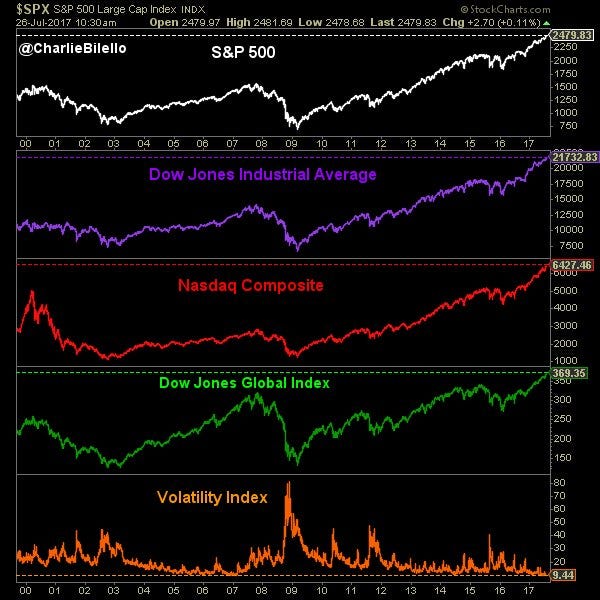

- record-low volatility on stock exchanges (US, Europe, Japan, ..)

- inflation hard to get on desired 2%

- stock indices rising for 8+ years like everything is doing great:

All these aspects are in place since the last big crisis, the financial crisis of 2007/2008. And I’m not even mentioning the amount of bonds the Bank of Japan currently owns, or the non-performing loans in China, or the private debt-positions in the US, China, Japan and Europe. It is the new normal that even though Microsoft sits on a huge pile of cash of $100bln, when buying LinkedIn for USD 26bln they took on a loan.

We are currently experiencing a multitude of exceptional and unprecendented concurrent circumstances, in our globalized economy. Despite the measures taken to prevent another crisis, we have not returned to a healthy post-crisis economic situation at all. How did we actually get here?

The dissociation of capital allocation from the economy: a play in three stages

The IT-era has given us a really strange new reality: an actual new dimension for information to travel in. Originally, information could only travel a distance over some (correlated) period of time, and at some significant cost. But the current data-infrastructure of the internet and intranets now allow information to travel without the traditional limitations of time and space. Information can now travel in unlimited ways and without any significant energy-consumption.

Just for convenience, let’s call this new dimension (or space) ‘D5’, since it is (for informational transactions) the dimension above the 3 spatial dimensions and the dimension of time (in physics usually the 4th dimension). It is like a wormhole-dimension for information.

It facilitates informational and transactional hyper-entropy.

Obviously, its impact on our real world cannot be underestimated. It is a revolution that eclipses the information-revolutions of the Gutenberg printing era and the radio/television/telephone era. It is everything from spreadsheets to internet (social media, wiki’s, webshops, online banking, email, torrents, news, etc), financial trading, and the latest technological advances in deep learning, IoT, big data, crypto, etc).

But on a very abstract level, the emergence of this new medium for information to travel in has had only few consequences:

- the migration of existing informational transactions into D5

- the creation of new (kinds of) informational transactions within D5

The astonishingly fast growth of accessible space in D5 has caused huge (and still ongoing) disruptive redistributions of all kinds of existing economic, financial and social transactions. A very obvious one is the reshuffeling of the traditional music-industry by online music-on-demand services. At some point, Apple made more money selling music than with selling their own products. Advertising is another great example where information technology completely alters the dynamics of an existing sector (a great book on this subject is Attention Merchants). Consolidation is still not converging, as it is constantly disrupted by new emerging technologies (AI, big data, health tech, IoT, fintech, crypto, etc).

The financial sector as main attractor

Of course, the financial sector has shown the usual extremities in flooding such a new medium, and it’s dragging everything with it, as it became an unprecedented instance of a ‘strange attractor’, globally. A ‘strange attractor’ is a mathematical concept (from complex-dynamic system theory). It designates a dynamic in which some structure in a compound environment (with lots of different actors) pulls a type of energy towards itself, causing all kinds of complex interactions. A low-pressure region in meteorology can be seen as such an attractor, since it pulls surrounding air towards it, and strong versions can cause hurricanes, creating turmoil in air-pressure, temperature and vapour, etc. And there are even much more complex versions, with multiple attractors, etc. In our globalized economy, several of these complex attractors have emerged.

So how did the financial sector become such a dominant attractor?

Structural dissociation by financialization

In a capitalist economy, a lot of capital is allocated into areas where there is an expected yield, a return on investment. Usually, these are investments in companies (through bank-loans/buying stocks), government bonds, commodities, currency-markets, etc. These are all investments in real economic markets, with (in principle) transparent and natural price-discovery mechanisms.

The IT-era, however, has facilitated a lot of new investment possibilities, and I would like to distinguish three subsequent but different trends in which these have emerged:

- the entrance of non-financial parties onto the financial markets, since the 1980's. These include consumers, public and semi-public institutions like housing corporations, schools, pension funds, etc. Some companies that entered these markets even made more money with speculative investing than with their own primary activities. And it’s still here: currently, the 4 biggest European carmakers, have €400bln in lending/leasing on their balances (which has doubled since financial crisis).

- the development of new financial markets, since the 1990’s. Commercial banks developing and trading ever new derivatives. The creativity in repackaging existing mortgages (CDO’s), the boom in ETF’s (index-trackers, funds, etc), insurances (CDS’s), etc. Also, the emergence of parties only making money with speculation and predation, such as hedge funds and high frequency traders (HFT). It is important to note that these are all parties and activities that get their yield only from within the financial sector, without having any association with the real economy.

- the entrance of central banks as key players in the financial market. Since 1987, the FED started to ‘play’ the stock-markets, in order to flatten the bust-boom cycles and ‘prevent’ new economic crises. But actually, they obfuscated existing price discovery mechanisms for stocks-markets, and tried to manipulate the natural business-cycles into linear trends. And currently they are trying to keep the financial markets in place with extreme manipulative measures (QE, ZNIRP). It is the most extreme version of dissocation of the financial markets from the real economy: it is playing the financial markets for the sake of the financial markets.

So actually, these are three stages in the dissociation of the financial domain from the economic domain, by the use of D5. And all these stages have shifted more capital allocation from the real world into the virtual world of the IT-infrastructure of D5, and have created huge amounts of interconnectivity within D5 itself, as well as between the real world and D5.

The financial sector has created lots of strange attractors (with its migration to D5), pulling all kinds of transactions towards it. A profound illustration of how hyper-entropy disturbs real-world entropy, is found at the stock exchanges. There, the very ultimate boundaries of hyper-entropy are challenged by the high frequency traders, causing a huge complex slipstream in both the real world and D5. From this perspective, the electronic exchanges can be seen as strange attractors.

A point of no return

Some analysts have been warning for the next crash (car-loans, the collapse of the Chinese economy, the bubble in the stock-markets, fracking/shale bubble, etc), or worse (geo-political crises, currency-wars, etc).

But whatever happens, it seems that every new technology, every bursting bubble, every natural disaster and every new policy just triggers the same response: pushing more capital into D5.

Credit is only expanding: central-bank balances have exploded (US/EU/Japan), and the US debt-ceiling has been raised again. Student-loans, car-loans, mortages, the examples are everywhere. Both public and private debt are continuously rising. It is all pushing more capital in D5. And investors are scavenging the areas where there might still be some real economic value, and are instantly creating new wormholes for it in D5 for some extra leverage.

For many, D5 is still the only place left to get some yield.

And because it is more expensive to bring stuff back to the real economy, it seems like a one-way street, as if the gravity sits in D5. As if the hyper-entropy dictates that the originally pristine D5 will be polluted (because it is cheaper to pollute than to pollute the real economy), until it reaches some saturation point. A point where the creation of new connections within D5 is more expensive than its potential return. A point where the scavenging of untouched areas is too expensive, like deep oil-wells. And where inflating new pointpotential bubbles is too expensive as well.

And this is the point where the whole system truly holds itself hostage, where no event can cause a systemic collapse anymore, or a significant crash. Things will barely move. Volatility will be minimal. We will be in standing water.

Hyper-entropy is ultimately resulting in congested entropy.

This the situation that all actions have lost impact. Financial policies will have no effect and all real price discovery is compromised. Real and fake news cannot be discerned anymore. Online discussions do not converge anymore. New online marketing-technologies will have no effect anymore. Everything becomes a snowflake. Actions just dissipate without traces, and new information is just more noise. True saturation, standing waters. This is not the crisis of catastrophe, but of congested equilibrium, holding itself hostage.

Things can barely move anymore because too much things could suddenly move too much. A crisis of entropy.

We are not here yet, but this seems to be the trend. And we may very well have to reach such a point of saturation before it is possible for things to reverse.

What’s next?

The thesis of this first part is that the IT-revolution actually serves as an extreme entropic accellerant for existing (macro socio-economic) trends, which disables any kind of (financial) policy and converges into some unnatural (and economically, socially and environmentally unhealthy) equilibrium.

Part 2 of this series will look into so-called High Frequency Trading as the most extreme version of all our crises. Also, it will investigate if asymmetric access to D5 allows for leveraging the existing asymmetric distribution of capital allocation.

Part 3 of this series will examine possible scenario’s after a saturation-point.

Note: I am not saying that the IT-revolution is a bad thing. I am just trying to understand what is going on from a purely systemic point of view. This blog is added to the Web11-publication since Web11 actually tries to prevent and mitigate these types of pollution.